Calculator Accuracy & Audit-Grade Verification

Form 8621 compliance is not merely a tax filing task; it is a data science problem.

It requires the serialization of irregular financial history into strict statutory logic. For the independent filer or tax professional, the goal is not just to fill a box on a form, but to produce a result that is mathematically deterministic and independently reproducible.

At 8621calculator.com, we treat our calculation engine as Compliance Infrastructure. We do not build "estimators." We build audit-grade computational engines designed to withstand the scrutiny of an algorithmic audit.

This document outlines the technical specifications of our engine, defining how we handle daily allocation, currency serialization, and statutory interest strictly according to the Internal Revenue Code (IRC).

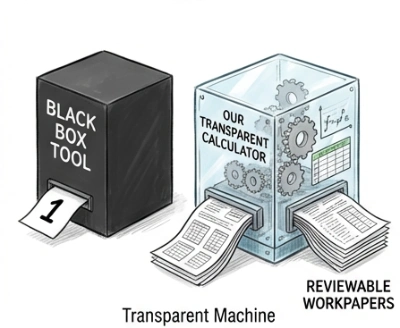

Compliance Infrastructure: This is Not a Toy

Most "PFIC calculators" online are simple estimators that mask complexity. For a Mathematically Independent Filer, an estimator is a liability. Form 8621 requires compliance infrastructure—an engine that produces substantiation workpapers and reproducible results.

This article demonstrates how to audit the calculation engine's adherence to the IRS technical compliance requirements for §1291 (Excess Distributions).

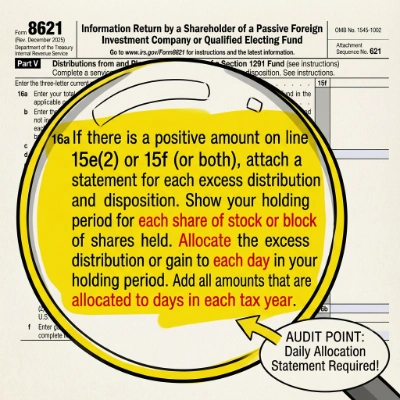

Audit Point 1: Line 16a Daily Allocation

Form 8621 Line 16a is a clinical outcome of Day-Weighted Allocation. The IRS requires a supporting statement showing exactly how income was distributed across the holding period.

Instructions for Form 8621 (Rev. December 2025)

IRS Official Mandate: Lines 16a and 16b

Determine the taxation of the excess distribution on a separate sheet and attach it to Form 8621. Divide the amount on line 15e(2) or 15f, whichever applies, by the number of days in your holding period. The holding period of the stock is treated as ending on the date of the distribution or disposition.

Special rules apply to the holding period if:

- The deemed dividend election (Election E) is made. See the instructions earlier for Election E.

- The mark-to-market election (Election C) is made or was made in a prior year (see section 1291(a)(3)(A)(ii)).

- The deemed dividend election with respect to a Section 1297(e) PFIC (Election G) or with respect to a Former PFIC (Election H) is made. See the instructions for Election G and Election H, earlier.

Determine the amount allocable to each tax year in your holding period by adding the amounts allocated to the days in each such tax year. Add the amounts allocated to the pre-PFIC and current tax years. Enter the sum on line 16b.

This amount is treated as ordinary income (for example, individuals and corporations should enter this amount on the “other income” line of their tax return).

Line 16a supporting statement: Daily allocation, annual aggregation, and per-lot tracking.

§1291 Sample Workpapers (ZIP)

Reference: IRS Form 8621 (December 2025)

| IRS Mandate (Instructions) | Clinical Significance / Audit Focus |

|---|---|

| "Attach a statement..." | Audit Focus: A missing or defective attachment can prevent the statute of limitations from starting under IRC §6501(c)(8). |

| "For each share or block" | Math Focus: Aggregating by "year" is non-compliant. Calculations must be performed per-lot to establish unique base periods. |

| "Allocate... to each day" | Precision: Mid-year approximations are ineligible. The engine must allocate income precisely over 365 (or 366) days per year. |

| "Add amounts... by tax year" | Verification: Daily allocations must be aggregated into annual totals before applying historic marginal tax rates. |

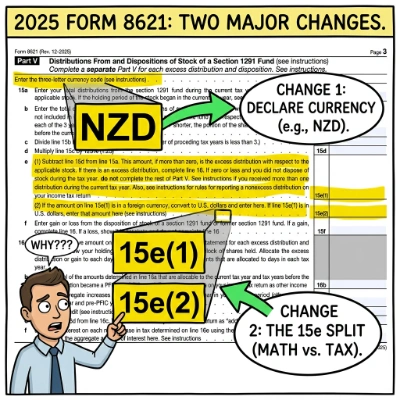

Audit Point 2: Line 15e Dual Currency (2025 New Rule)

The 2025 revision of Form 8621 does not change the underlying foreign-currency computation rules for Line 15e; instead, it makes the dual-currency workflow explicit by requiring separate reporting of the distribution-currency amount and its U.S. dollar translation.

Verification: Confirm that transaction-date currency translation uses daily spot exchange rates (this calculator uses OANDA daily exchange rates).

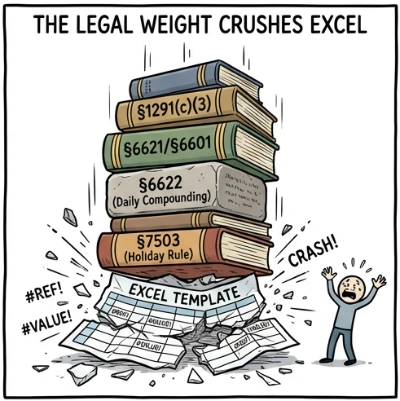

Audit Point 3: §6621/§6622/§7503 Interest Logic

The PFIC Section 1291 interest computation is governed by four distinct legal frameworks that collectively constrain the calculation to Audit-Grade Accuracy:

- IRC §1291(c)(3): Defines the interest period.

- IRC §6621/§6601: Defines historical quarterly underpayment rates.

- IRC §6622: Mandates Daily Compounding.

- IRC §7503: Adjusts due dates for weekends and federal holidays.

A clinical engine must account for weekend/holiday adjustments. If a tax deadline falls on a Sunday, the interest start date shifts—this is a professional-level detail required for true accuracy.

View Historical Statutory Filing Deadlines (IRC §7503 Adjustments)

Under IRC §7503, if a tax deadline falls on a Saturday, Sunday, or legal holiday, the performance of the act shall be considered timely if performed on the next succeeding day which is not a Saturday, Sunday, or legal holiday.

View Historical IRS §6621 Underpayment Rates (1987–Present)

These rates are used for the daily compounding interest calculations under §1291(c). Rates are updated quarterly by the IRS.

| Year | Q1 | Q2 | Q3 | Q4 |

|---|---|---|---|---|

| 2026 | 7% | 7% (Estimated) | - | - |

| 2025 | 7% | 7% | 7% | 7% |

| 2024 | 8% | 8% | 8% | 8% |

| 2023 | 7% | 7% | 7% | 8% |

| 2022 | 3% | 4% | 5% | 6% |

| 2021 | 3% | 3% | 3% | 3% |

| 2020 | 5% | 5% | 3% | 3% |

| 2019 | 6% | 6% | 5% | 5% |

| 2018 | 4% | 5% | 5% | 5% |

| 2017 | 4% | 4% | 4% | 4% |

| 2016 | 3% | 4% | 4% | 4% |

| 2015 | 3% | 3% | 3% | 3% |

| 2014 | 3% | 3% | 3% | 3% |

| 2013 | 3% | 3% | 3% | 3% |

| 2012 | 3% | 3% | 3% | 3% |

| 2011 | 3% | 4% | 4% | 3% |

| 2010 | 4% | 4% | 4% | 4% |

| 2009 | 5% | 4% | 4% | 4% |

| 2008 | 7% | 6% | 5% | 6% |

| 2007 | 8% | 8% | 8% | 8% |

| 2006 | 7% | 7% | 8% | 8% |

| 2005 | 5% | 6% | 6% | 7% |

| 2004 | 4% | 5% | 4% | 5% |

| 2003 | 5% | 5% | 5% | 4% |

| 2002 | 6% | 6% | 6% | 6% |

| 2001 | 9% | 8% | 7% | 7% |

| 2000 | 8% | 9% | 9% | 9% |

| 1999 | 7% | 8% | 8% | 8% |

| 1998 | 9% | 8% | 8% | 8% |

| 1997 | 9% | 9% | 9% | 9% |

| 1996 | 9% | 8% | 9% | 9% |

| 1995 | 9% | 10% | 9% | 9% |

| 1994 | 7% | 7% | 8% | 9% |

| 1993 | 7% | 7% | 7% | 7% |

| 1992 | 9% | 8% | 8% | 7% |

| 1991 | 11% | 10% | 10% | 10% |

| 1990 | 11% | 11% | 11% | 11% |

| 1989 | 11% | 12% | 12% | 11% |

| 1988 | 11% | 10% | 10% | 11% |

| 1987 | 9% | 9% | 9% | 10% |

Note: These reflect the Underpayment Rates for individual taxpayers.

Source: IRS Quarterly

interest rates

§6621 Interest Underpayment Verifier

An algorithmic proof of our calculation engine. Verify §6621/§6622 daily compounding logic against IRS standards.

Clinical Readiness Assessment

Form 8621 DIY is a powerful path to mathematical independence, but it requires high data integrity. Reconsider independent filing if:

- You cannot produce a clean CSV of every purchase and sale (see the Calculator Quick Start Guide).

- Prior-year filings contain known errors (e.g. Missed vs. Incorrect Reporting).

- PFIC balances exceed your personal risk/complexity threshold.

Defect Bounty & Refund Policy

We do not ask for "trust"; we provide mathematical certainty. Our refund policy is effectively a Technical Accuracy Guarantee:

If a provable mathematical error—established using identical inputs and referencing specific IRC sections (e.g. §1291 case studies)—is found in the engine's output, a full refund is provided.

We treat technical discrepancies as defect reports, not support issues. This commitment to clinical precision is why this engine is used by Independent Filers who require audit-grade reproducibility.

The Takeaway

Reproducibility is the ultimate standard of truth.

A transparent, reviewable calculation—backed by substantiation workpapers—is the only way to file Form 8621 with absolute confidence.

- Verify one controlled PFIC first using a manual calculation as a benchmark.

- Compare workpapers against historic filed results (if available).

- Confirm spot-rate and daily-allocation logic for adherence to the IRS technical requirements.

- Establish your own clinical audit trail.

Use this workflow as your personal Form 8621 validation tool before submitting to the IRS.